Nov 12, 2019

Nov 12, 2019

5 Tips for Efficient Commercial Loan Origination

Post-recession lending has been very good for businesses, especially small businesses needing a loan. Community-based, commercial lenders have taken up a lot of the space that large, national banks used to hold among small business lending because of their ability to know their customers, the industry, and the community and, as a result, construct unique deals. How can financial institutions make commercial loan origination more efficient?

Here are five tips you need to know about improving commercial lending operations.

1. Use Technology Wisely

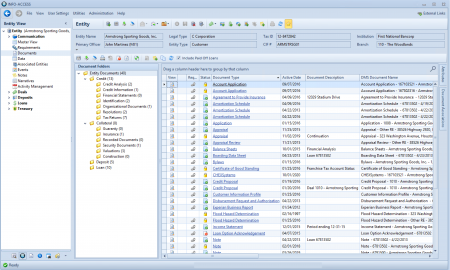

Credit origination, tracking, servicing, and business intelligence software has become essential in the world of lending. Using powerful CRM software can ensure that you measure each customer’s relationship with your institution over time. By tracking their behavior and your interactions with them, you’ll limit risk and maximize your relationships.

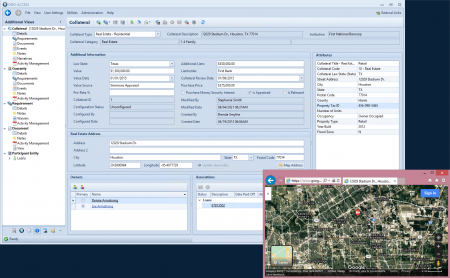

Watching credit limits and getting regular exposure reporting gives you a bird’s eye view of your borrowers. Keeping an eye on their financial performance, facility structuring, and risk ratings can help you avoid deterioration in credit quality. And, robust collateral management software allows your institution to assess cross-collateralizations and loan-to-value adequacy accurately, and to identify and manage concentrations of credits by loan types, collateral types, industry types, or even concentrations of loans within a specific development project.

2. Stay Transparent and Consistent

In most cases, the process for underwriting loans is still manual, especially in the commercial lending space because every loan is unique, but entering data into spreadsheets, cross-checking it, and drawing a conclusion is time-consuming. This process can result in inconsistencies in underwriting and even show a lack of transparency.

Using a state-of-the-art loan origination and management system built to work for commercial lending and the complexities each new deal brings can help you to standardize your underwriting process, even for complex, commercial lending. It puts consistent data on a common platform so that your staff can see it when they need it. Instead of shuffling data, information, and communication through disjointed tools or managing through cluttered inboxes, everything is available to your team when they need it.

3. Strategy Matters

Inefficient operations can no longer fly in today’s financial environment. With increasing regulatory burden and compressed margins, remaining competitive, strong, and profitable is more challenging than ever before. Institutions unable or unwilling to invest capital in technological solutions and the personnel resources to maintain clean, thorough, integrated systems will be forced to increase staffing levels to support antiquated processes that will carry far greater costs in the long run.

When you’re managing for continued growth, you need to implement new systems that can sustain your organizational and operational changes. Many companies use adaptations of their previous paper systems to try to manage vast amounts of digital data. The best institutions realize when it’s time to upgrade to leverage technology rather than balloon their personnel budget.

4. Maintain a 360-degree View

One of the most important changes in loan origination is the way that risk concentrations are measured and identified. When lenders and management are unable to identify these concentrations of risks for borrowers, heavy losses can occur.

Lenders today are oftentimes using manually updated spreadsheets to track positions. Adding up numbers from multiple systems is no longer a viable way to work. Efficient and effective portfolio risk management requires a much more reliable solution that’s not subject to human error.

Choosing a comprehensive technological solution allows you to fully leverage the integrations, analysis, and streamlined workflows available so you can cut down on the time it takes to fund a loan. Streamlined borrower analysis can improve your customer service by approving a loan in one-third less than it would normally take you.

5. Focus on Service

Marketplace lenders do well simply because they focus on customer service. Their models are built on the new technology that everyone is using. They maintain seriously fast response times that other lenders can’t offer, but they must stick to narrow lending opportunities to do so.

The efficiency of a modern system needs to be harnessed by community financial institutions. Faster responses coupled with the ability to provide custom financing terms for your borrowers’ unique situation (a long-time strength of local institutions) means that you’re winning customers over more often.

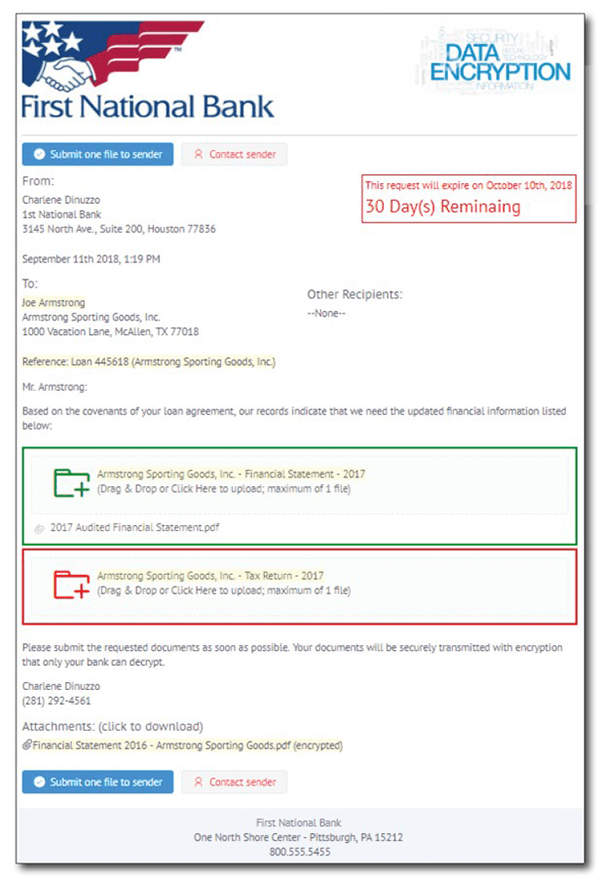

Consider paperless loan underwriting as one of the answers to your problems. The way that technology has evolved now allows for lenders and loan originators to move toward paperless processes. Traditional loan origination requires so much paperwork that a lot of mistakes, as well as lost or misplaced documents, can occur in the process. While document handling should no longer be a worry for any lending team, the reality is that if you aren’t managing your documents and tracking smarter, your lending process is not going to be as fast as it could. There are enough tools now that if you’re not fully paperless already, you should be on your way.

Blow Competitors Away

By embracing technology and streamlining your processes, rather than slowing things down with old systems, it’s possible for everyone to succeed. Not only will small businesses be well served, but commercial lenders will share in the profits.

Carefully evaluate potential systems to make sure you get the most bang for your buck. A thorough solution should be able to provide a customer communication and document sharing portal; credit proposal prep and underwriting tools; integrated document and requirement policy, and exception tracking; integrations with your document prep software, core, and DMS; analysis tools; business intelligence dashboards and automated work notifications; and audit and compliance trails. Without a total solution, you run the risk of having to purchase multiple systems, increasing costs, setup efforts, and application management time and introducing the possibility of lost efficiencies through disparate systems.

Bookmark our site to ensure that you’re on top of all the major changes to come for commercial lenders, and learn about our solution geared specifically to work with the complexities of commercial lending: PRO-ACCESS.